Friday, December 29, 2017

Thursday, December 28, 2017

Top 10 Do-It-Yourself Home Improvements

What's your number one goal when selling your home? For most homeowners it's selling it for what it's worth, especially if you've invested a lot of time and effort into updating it. Here are 10 DIY home improvement projects that will give you the highest return on investment.

Wednesday, December 27, 2017

Tuesday, December 26, 2017

9 Easy Mistakes Homeowners Make on Their Taxes

Don’t rouse the IRS or pay more taxes than necessary — know the score on each home tax deduction and credit.

The federal tax law signed by President Donald Trump Dec. 22, 2017, may affect home ownership tax benefits described in this article. The new law goes into effect for the 2018 tax year and generally doesn’t affect tax filings for the 2017 tax year.

As you calculate your tax returns, be careful not to commit any of these nine home-related tax mistakes, which tax pros say are especially common and can cost you money or draw the IRS to your doorstep.

#1 Deducting the Wrong Year for Property Taxes

You take a tax deduction for property taxes in the year you (or the holder of your escrow account) actually paid them. Some taxing authorities work a year behind — that is, you’re not billed for 2013 property taxes until 2014. But that’s irrelevant to the feds.

Enter on your federal forms whatever amount you actually paid in that tax year, no matter what the date is on your tax bill. Dave Hampton, CPA, a tax department manager at the Cincinnati accounting firm of Burke & Schindler, has seen homeowners confuse payments for different years and claim the incorrect amount.

#2 Confusing Escrow Amount for Actual Taxes Paid

If your lender escrows funds to pay your property taxes, don’t just deduct the amount escrowed. The regular amount you pay into your escrow account each month to cover property taxes is probably a little more or a little less than your property tax bill. Your lender will adjust the amount every year or so to realign the two.

For example, your tax bill might be $1,200, but your lender may have collected $1,100 or $1,300 in escrow over the year. Deduct only $1,200 or the amount of property taxes noted on the Form 1098 that your lender sends. If you don’t receive Form 1098, contact the agency that collects property tax to find out how much you paid.

#3 Deducting Points Paid to Refinance

Deduct points you paid your lender to secure your mortgage in full for the year you bought your home. However, when you refinance, you must deduct points over the life of your new loan.

For example, if you paid $2,000 in points to refinance into a 15-year mortgage, your tax deduction is $2,000 divided by 15 years, or $133 per year.

#4 Misjudging the Home Office Tax Deduction

The deduction is complicated, often doesn’t amount to much of a deduction, has to be recaptured if you turn a profit when you sell your home, and can pique the IRS’s interest in your return.

But there’s good news. There’s a new simplified home office deduction option if you don’t want to claim actual costs. If you’re eligible, you can deduct $5 per square foot up to 300 feet of office space, or up to $1,500 per year.

#5 Failing to Repay the First-Time Homebuyer Tax Credit

If you used the original homebuyer tax credit in 2008, you must repay 1/15th of the credit over 15 years.

If you used the tax credit in 2009 or 2010 and then within 36 months you sold your house or stopped using it as your primary residence, you also have to pay back the credit.

The IRS has a tool you can use to help figure out what you owe.

#6 Failing to Track Home-Related Expenses

If the IRS comes a-knockin’, don’t be scrambling to compile your records. File or scan and store home office and home improvement expense receipts and other home-related documents as you go.

#7 Forgetting to Keep Track of Capital Gains

If you sold your main home last year, don’t forget to pay capital gains taxes on any profit. You can typically exclude $250,000 of any profits from taxes (or $500,000 if you’re married filing jointly).

So if your cost basis for your home is $100,000 (what you paid for it plus any improvements) and you sold it for $400,000, your capital gains are $300,000. If you’re single, you owe taxes on $50,000 of gains.

However, there are minimum time limits for holding property to take advantage of the exclusions, and other details. Consult IRS Publication 523. And high-income earners could get hit with an additional tax.

#8 Filing Incorrectly for Energy Tax Credits

If you made any eligible improvements in 2015 and 2016, such as installing energy-efficient heating and cooling system, you may be able to take a 10% tax credit, up to $500. With some systems your cap is lower than $500. For instance, you can only claim $200 on windows. But keep in mind, this is a lifetime credit. If you claimed the credit in any recent years, you’re done.

Installing a solar electric, solar water heater, geothermal, or small wind energy system can also make you eligible to take the Residential Energy Efficient Property Credit.

To claim the deduction, you have to use the complicated Form 5695, which can mean cross-checking with half a dozen other IRS forms. Read the instructions carefully.

#9 Claiming Too Much for the Mortgage Interest Tax Deduction

Taxpayers are allowed to deduct mortgage interest on home acquisition debt up to $1 million, plus they can also deduct up to $100,000 in home equity debt.

This article provides general information about tax laws and consequences, but shouldn’t be relied upon as tax or legal advice applicable to particular transactions or circumstances. Consult a tax professional for such advice.

Friday, December 22, 2017

Existing Home Sales Reach Highest Annual Pace in 11 Years

Existing home sales are currently at an annual pace of 5.81 million, the highest pace since December 2006. The inventory of existing homes for sale has dropped year-over-year for the last 30 consecutive months and is now at a 3.4-month supply. NAR’s Chief Economist Lawrence Yun had this to say: “Faster economic growth in recent quarters, the booming stock market and continuous job gains are fueling substantial demand for buying a home as 2017 comes to an end.”

Thursday, December 21, 2017

Happy Holidays!

'Twas

the night before closing when all thro' the office, not an agent was

sweating, not even the bosses. The contracts were scanned by the space

heater with care, in hopes that the clear to close soon would be

there.The client gifts are nestled all snug in the car, while visions of

signatures dance among the stars. And the title company with all the

documents and I with the champagne, when the clients close their

checkbook we hope for no chest pains. As the Realtor lays their head to

rest, dreaming of all parties driving off into the sunset.  🎄

🎄

Happy closings to all and to all don't forget... I'm never too busy for your referrals!

www.timgrissett.com

Happy closings to all and to all don't forget... I'm never too busy for your referrals!

www.timgrissett.com

5 Home Improvement Projects to Avoid

Whether you're doing a complete remodel or making a small upgrade, be sure to consider whether any potential projects will offer you maximum return on your initial investment. If you plan on moving in two to five years don't invest money in home improvement projects that won't increase the resale value of your home.

Wednesday, December 20, 2017

Tuesday, December 19, 2017

Monday, December 18, 2017

Friday, December 15, 2017

Thursday, December 14, 2017

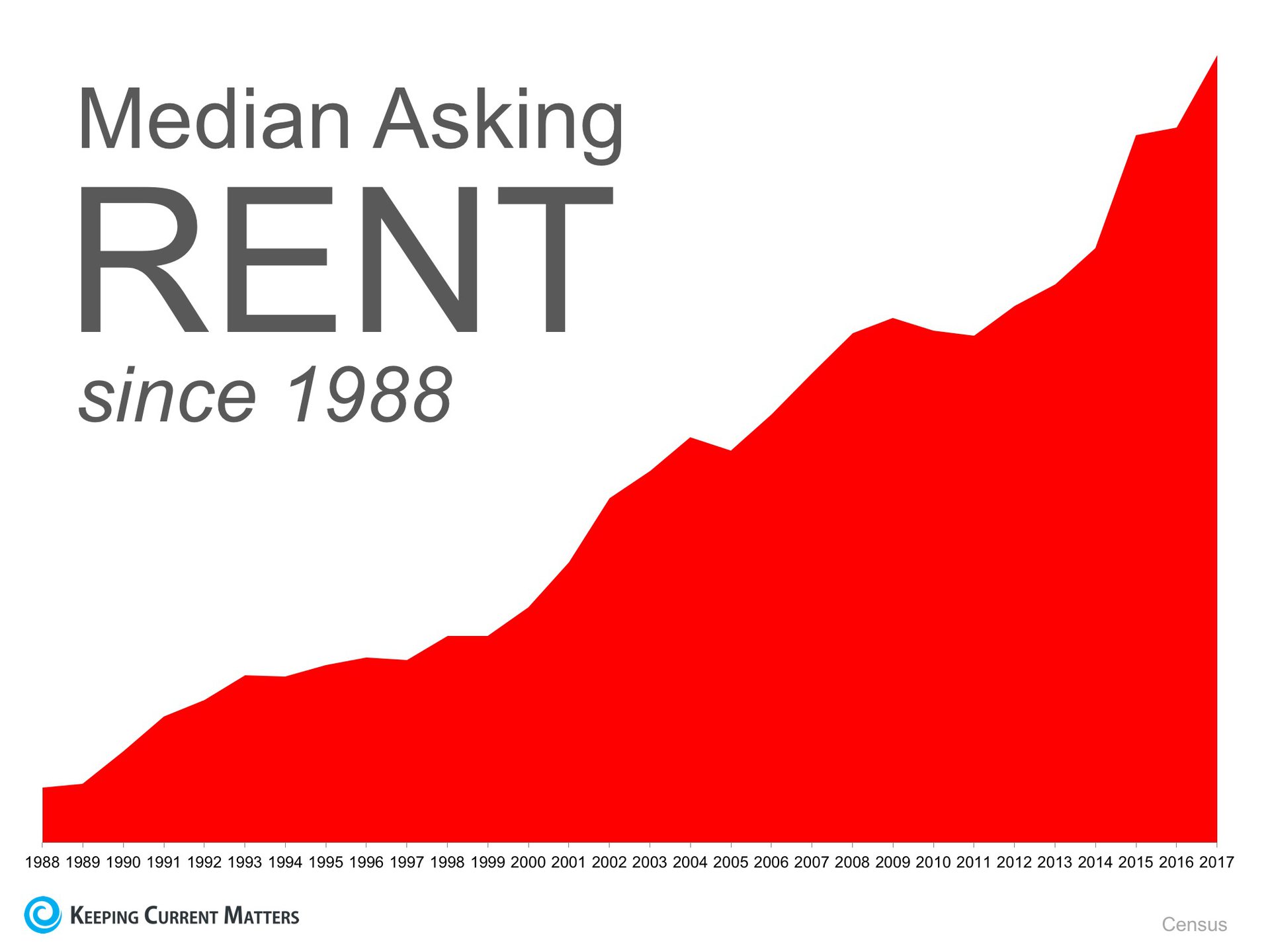

Should Boomers Buy or Rent after Selling?

In a recent CNBC article, it was reported that many baby boomers are selling their current homes and moving into rentals, rather than purchasing another home.

“Between 2009 and 2015, the number of renters aged 55 or above rose 28 percent, while those aged 34 or younger only increased 3 percent…This makes sense in the short term for many reasons. If you are moving to a different part of town or a new region of the country, you may decide to rent until you pick the perfect home in an area you love. However, is renting a good long-term strategy?

Meanwhile, more than 5 million baby boomers across the nation are expected to rent their next home by 2020, according to a 2016 analysis from Freddie Mac.”

A mortgage payment remains fixed. Rents, however…

The Census Bureau recently released their 2017 third quarter median rent numbers. Here is a graph showing rent increases from 1988 until today:

As you can see, rents have steadily increased and are showing no signs of slowing down. If you are faced with making the decision of whether you should rent or buy your next home, you should take this into consideration.

Bottom Line

One way to protect yourself from rising rents is to lock in your housing expense by buying a home instead of renting. Meet with a local real estate professional who can help you decide what the best step is for you and your family!

Wednesday, December 13, 2017

HOME MAINTENANCE

Your

home is likely your biggest investment. You use it every day. It’s

important. Despite these facts, many of us struggle to keep up with

important maintenance tasks that are really essential for retaining our

home’s value. When it comes to home maintenance, paying attention to the

little things can save you lots of money, time and house-repair

headaches.

A Home Is A Leveraged Investment

The name of the game in building wealth is leverage. Once you understand it, know how to use it, and do so often, you’ll build wealth faster and far more effectively. Part of the problem for most people is that they simply don’t understand how to build wealth. Stocks, bonds, 401(k)s, real estate – those can all be PIECES of the wealth puzzle.

However, the piece of the puzzle most people are missing is LEVERAGE. Focusing on leverage will fast track your wealth creation.

Tuesday, December 12, 2017

Before You Make an Offer, Here Are 4 Tips for Success!

So, you’ve been searching for that perfect house to call a ‘home,’ and you finally found it! The price is right, and in such a competitive market, you want to make sure that you make a good offer so that you can guarantee that your dream of making this house yours comes true!

Freddie Mac covered “4 Tips for Making an Offer” in their Executive Perspective. Here are the 4 tips they covered along with some additional information for your consideration:

1. Understand How Much You Can Afford

“While it’s not nearly as fun as house hunting, fully understanding your finances is critical in making an offer.”This ‘tip’ or ‘step’ should really take place before you start your home search process.

Getting pre-approved is one of many steps that will show home sellers that you are serious about buying, and will allow you to make your offer with the confidence of knowing that you have already been approved for a mortgage for that amount. You will also need to know if you are prepared to make any repairs that may need to be made to the house (ex: new roof, new furnace).

2. Act Fast

“Even though there are fewer investors, the inventory of homes for sale is also low and competition for housing continues to heat up in many parts of the country.”The inventory of homes listed for sale has remained well below the 6-month supply that is needed for a ‘normal’ market. Buyer demand has continued to outpace the supply of homes for sale, causing buyers to compete with each other for their dream homes.

Make sure that as soon as you decide that you want to make an offer, you work with your agent to present it as soon as possible.

3. Make a Solid Offer

Freddie Mac offers this advice to help make your offer the strongest it can be:“Your strongest offer will be comparable with other sales and listings in the neighborhood. A licensed real estate agent active in the neighborhoods you are considering will be instrumental in helping you put in a solid offer based on their experience and other key considerations such as recent sales of similar homes, the condition of the house and what you can afford.”Talk with your agent to find out if there are any ways that you can make your offer stand out in this competitive market!

4. Be Prepared to Negotiate

“It’s likely that you’ll get at least one counteroffer from the sellers so be prepared. The two things most likely to be negotiated are the selling price and closing date. Given that, you’ll be glad you did your homework first to understand how much you can afford.If your offer is approved, Freddie Mac urges you to “always get an independent home inspection, so you know the true condition of the home.” If the inspector uncovers undisclosed problems or issues, you can discuss any repairs that may need to be made with the seller, or cancel the contract.

Your agent will also be key in the negotiation process, giving you guidance on the counteroffer and making sure that the agreed-to contract terms are met.”

Bottom Line

Whether you’re buying your first home or your fifth, having a local professional on your side who is an expert in their market is your best bet in making sure the process goes smoothly. Happy House Hunting!

Monday, December 11, 2017

Friday, December 8, 2017

3 Tips for Making Your Dream of Buying A Home Come True

Setting up an automatic savings plan that saves a small amount of every check is one of the best ways to save without thinking a lot about it. Living within a budget will not only help you save money for down payments but will help you pay down other debts that might be holding you back.

www.timgrissett.com

Thursday, December 7, 2017

It's Beginning to Look A Lot Like Christmas!

How

are you dressing your mantel for the holiday season? You know it's not

too late for Santa to bring you a new house for Christmas!

www.timgrissett.com

www.timgrissett.com

Wednesday, December 6, 2017

Tuesday, December 5, 2017

Don’t Let Inspections Become Deal-Breakers

A home inspection gone awry can spell double trouble in a real estate transaction. Sellers who believe they’ve kept their house in pristine condition might hit the roof when costly problems with the property are uncovered. And buyers—especially first-timers with no experience in the market—may be scared away by the prospect of daunting repairs.

How do you keep this common scenario from devolving into acrimony? Before the inspection, talk with your clients about their expectation and about how they might handle certain results, says Daniel L. Alden, broker-associate at William Pitt Sotheby’s International Realty in Great Barrington, Mass.

Listing agents can be proactive by doing a visual inspection of their client’s home, looking for obvious areas that need repair. Rich Wolnik Jr., a sales associate with Riklin Realty in Niles, Ill., advises reviewing the age of the seller’s furnace, water heater, and air conditioning unit and finding out what major repairs or upgrades have been done. Make sure sellers are aware of issues that are common in your market—such as termites in waterfront communities—and let them know that whatever issues you find in a visual inspection will very likely arise in an official inspection.

Sellers may want to pay for a prelisting inspection. This gives them an opportunity to collect cost estimates for repairs and determine whether they want to pay for fixes or lower their asking price. Either way, it can prevent last-minute setbacks.

Some sellers will balk at incurring the cost of a prelisting inspection. Brian Bartholomew, a sales associate with RE/MAX Cornerstone in Fullerton, Calif., offers to cover the cost—typically about $450—as a value-added benefit for clients who pay his usual commission. About half of his sellers opt for a prelisting inspection, he says.

As for buyers, they need to understand the difference between health and safety issues and normal wear and tear. When buyers are determined to make repairs part of the sales contract, suggest they offer options. For example, they could ask sellers to either have repairs done before move in or provide a credit on the price, says Sara McMurray, CIPS, SFR, a sales associate with Keller Williams Realty in Chicago.

If buyers’ first reaction to inspection problems is to walk away, remind them of why they were moved to make an offer in the first place. With inventory as tight as it is in many areas, they may rue letting inspection issues derail their dream. “If this is the only property you’ve seen that meets your requirements, let’s talk it through and make it work,” McMurray tells her clients.

Monday, December 4, 2017

5 Reasons to Sell This Winter!

Here are five reasons listing your home for sale this winter makes sense.

1. Demand Is Strong

The latest Buyer Traffic Report from the National Association of Realtors (NAR) shows that buyer demand remains very strong throughout the vast majority of the country. These buyers are ready, willing and able to purchase… and are in the market right now! More often than not, multiple buyers are competing with each other to buy a home.

Take advantage of the buyer activity currently in the market.

2. There Is Less Competition Now

Housing inventory is still under the 6-month supply that is needed for a normal housing market. This means that, in the majority of the country, there are not enough homes for sale to satisfy the number of buyers in the market. This is good news for homeowners who have gained equity as their home values have increased. However, additional inventory could be coming to the market soon.

Historically, the average number of years a homeowner stayed in their home was six, but has hovered between nine and ten years since 2011. There is a pent-up desire for many homeowners to move, as they were unable to sell over the last few years because of a negative equity situation. As home values continue to appreciate, more and more homeowners will be given the freedom to move.

The choices buyers have will continue to increase. Don’t wait until this other inventory comes to market before you decide to sell.

3. The Process Will Be Quicker

Today’s competitive environment has forced buyers to do all they can to stand out from the crowd, including getting pre-approved for their mortgage financing. This makes the entire selling process much faster and much simpler as buyers know exactly what they can afford before home shopping. According to Ellie Mae’s latest Origination Insights Report, the time to close a loan has dropped to 44 days, after seeing a 12-month high of 48 days in January.

4. There Will Never Be a Better Time to Move Up

If your next move will be into a premium or luxury home, now is the time to move up! The inventory of homes for sale at these higher price ranges has forced these markets into a buyer’s market. This means that if you are planning on selling a starter or trade-up home, your home will sell quickly, AND you’ll be able to find a premium home to call your own!

Prices are projected to appreciate by 4.7% over the next year according to CoreLogic. If you are moving to a higher-priced home, it will wind up costing you more in raw dollars (both in down payment and mortgage payment) if you wait.

5. It’s Time to Move on With Your Life

Look at the reason you decided to sell in the first place and determine whether it is worth waiting. Is money more important than being with family? Is money more important than your health? Is money more important than having the freedom to go on with your life the way you think you should?

Only you know the answers to the questions above. You have the power to take control of the situation by putting your home on the market. Perhaps the time has come for you and your family to move on and start living the life you desire.

That is what is truly important.

Friday, December 1, 2017

Best of Atlanta

This is Best of Atlanta! These are the restaurants, shops, and people that make Atlanta the best place to live. On newsstands now! http://bit.ly/2AwXFa5

Subscribe to:

Comments (Atom)