Wednesday, October 31, 2018

Taking Fear Out of the Mortgage Process

A considerable number of potential buyers shy away from jumping into the real estate market due to their uncertainties about the buying process. A specific cause for concern tends to be mortgage qualification.

For many, the mortgage process can be scary, but it doesn’t have to be!

In order to qualify in today’s market, you’ll need a down payment (the average down payment on all loans last year was 5%, with many buyers putting down 3% or less), a stable income, and good credit history.Throughout the entire home buying process, you will interact with many different professionals who will all perform necessary roles. These professionals are also valuable resources for you.

Once you’re ready to apply, here are 5 easy steps that Freddie Mac suggests to follow:

- Find out your current credit history & score – even if you don’t have perfect credit, you may already qualify for a loan. The average FICO Score® of all closed loans in September was 731, according to Ellie Mae.

- Start gathering all of your documentation – income verification (such as W-2 forms or tax returns), credit history, and assets (such as bank statements to verify your savings).

- Contact a professional – your real estate agent will be able to recommend a loan officer who can help you develop a spending plan, as well as help you determine how much home you can afford.

- Consult with your lender – he or she will review your income, expenses, and financial goals in order to determine the type and amount of mortgage you qualify for.

- Talk to your lender about pre-approval – a pre-approval letter provides an estimate of what you might be able to borrow (provided your financial status doesn’t change) and demonstrates to home sellers that you are serious about buying!

Bottom Line

Do your research, reach out to professionals, stick to your budget, and be sure that you are ready to take on the financial responsibilities of becoming a homeowner.Tuesday, October 30, 2018

Are You Spending TOO Much on Rent?

Chances are if you are renting you are spending too much of your income on your monthly housing expense. There is a long-standing ‘rule’ that a household should not pay more than 28% of their income on their rent or mortgage payment. This percentage allows the household to save money for the future while comfortably covering other expenses.

According to new data released from ApartmentList.com, 49.5 million renters in the United States were cost-burdened in 2017, meaning they spent more than 30% of their monthly incomes on rent. This accounts for nearly half of all renter households in the country and is up 3.1 million from 2007.

When a household is cost-burdened by their monthly housing expense, they are not as easily able to save money for the future. This is a big factor for many renters who dream of owning their own homes someday.

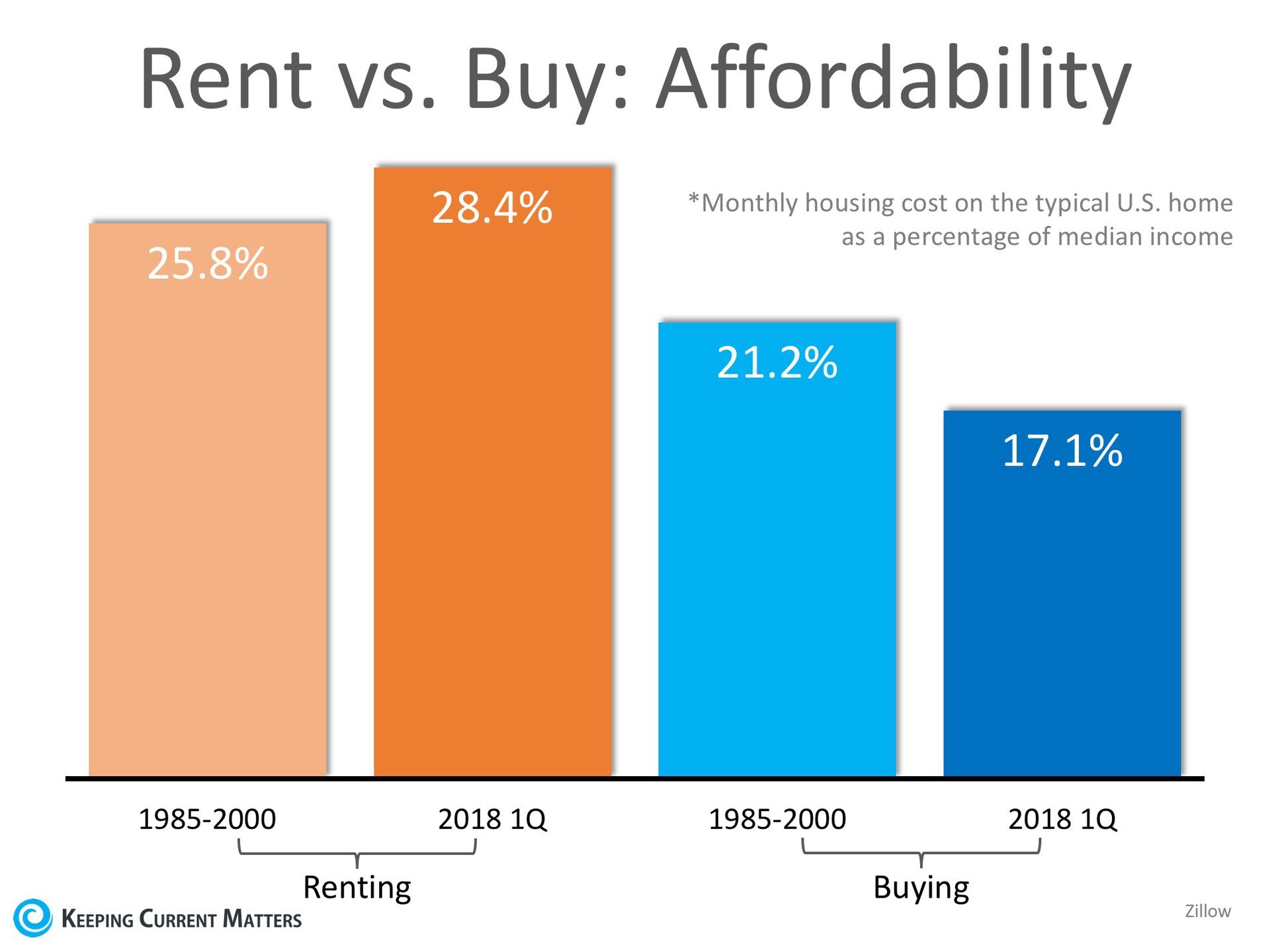

But there is hope for those who are able to save at least a 3% down payment! The percentage of income needed in the US to buy a home is significantly less than renting at 17.1%!

The chart below compares the historic percentage of income needed to rent and buy from 1985-2000 to the first quarter of 2018. As you can see, the cost of renting has climbed above historic numbers while the cost of buying dropped over the same period of time.

Bottom Line

If you are one of the many renters who is spending too much of their monthly income on rent, consider saving money by getting a roommate, moving into a less expensive apartment, or even moving in with family. These are all ways to save for a down payment so that you can put your housing costs to work for you!Monday, October 29, 2018

Thinking of Selling Your Home? Here's Why You Need A Pro in Your Corner

With home prices on the rise and buyer demand still strong, some sellers may be tempted to try and sell their homes on their own without using the services of a real estate professional.

Real estate agents are trained and experienced in negotiation and, in most cases, the seller is not. Sellers must realize that their ability to negotiate will determine whether or not they get the best deal for themselves and their families.

Here is a list of just some of the people with whom the seller must be prepared to negotiate with if they decide to For Sale by Owner (FSBO):

- The buyer who wants the best deal possible

- The buyer’s agent who solely represents the best interests of the buyer

- The buyer’s attorney (in some parts of the country)

- The home inspection companies, which work for the buyer and will almost always find some problems with the house

- The termite company if there are challenges

- The buyer’s lender if the structure of the mortgage requires the sellers’ participation

- The appraiser if there is a question of value

- The title company if there are challenges with certificates of occupancy (CO) or other permits

- The town or municipality if you need to get the CO permits mentioned above

- The buyer’s buyer in case there are challenges with the house your buyer is selling

Bottom Line

The percentage of sellers who have hired real estate agents to sell their homes has increased steadily over the last 20 years. Meet with a professional in your local market to see the difference that he or she can make in easing the selling process for you.

I am always at your service for real estate. At Halloween time or any time of the year! 👻🦇💀🕷🕸🎃⚰️

#realestate #home #halloween #newhome #dreamhome #realestateagent #firsttimebuyer

#realestate #home #halloween #newhome #dreamhome #realestateagent #firsttimebuyer

Friday, October 26, 2018

Buying a Home Can Be Scary… Until You Know the Facts

Many potential homebuyers believe that they need a 20% down payment and a 780 FICO® score to qualify to buy a home which stops many of them from even trying! Here are some facts:

72% of buyers who purchased homes this year have put down less than 20%.

76.4% of loan applications were approved last month.

The average credit score of approved loans was 727 in September.

Thursday, October 25, 2018

Where are Home Values Headed over the Next Few Years?

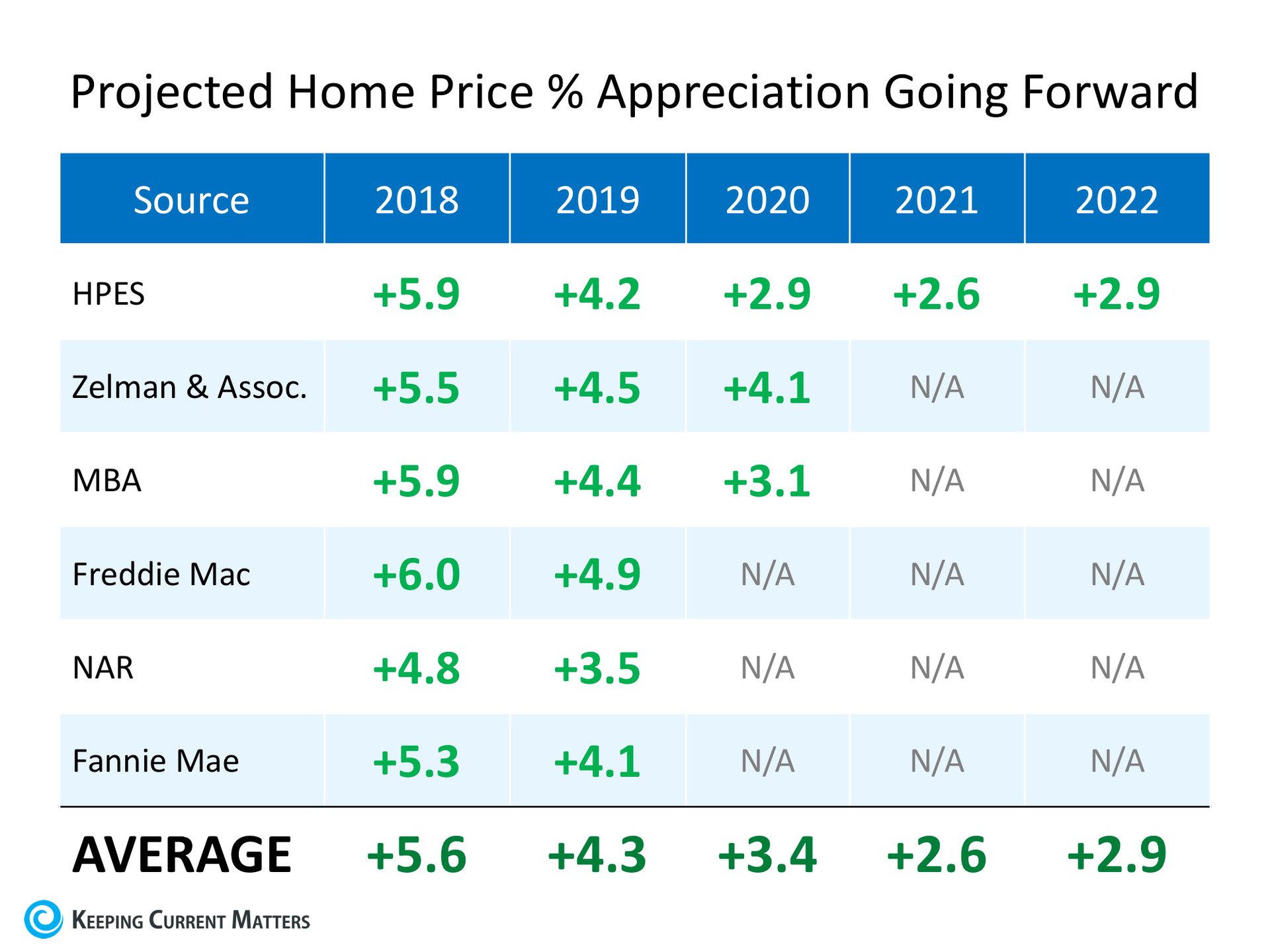

There are many questions about where home prices will be next year as well as where they may be headed over the next several years to come. We have gathered the most reliable sources to help answer these questions:

The Home Price Expectation Survey – A survey of over 100 market analysts, real estate experts, and economists conducted by Pulsenomics each quarter.

Zelman & Associates – The firm leverages unparalleled housing market expertise, extensive surveys of industry executives, and rigorous financial analysis to deliver proprietary research and advice to leading global institutional investors and senior-level company executives.

Mortgage Bankers Association (MBA) – As the leading advocate for the real estate finance industry, the MBA enables members to successfully deliver fair, sustainable, and responsible real estate financing within ever-changing business environments.

Freddie Mac – An organization whose mission is to provide liquidity, stability, and affordability to the U.S. housing market in all economic conditions extending to all communities from coast to coast.

The National Association of Realtors (NAR) – The largest association of real estate professionals in the world.

Fannie Mae – A leading source of financing for mortgage lenders, providing access to affordable mortgage financing in all markets always.

Here are their projections of prices going forward:

Bottom Line

Every source sees home prices continuing to appreciate – just at lower percentages as we move through the next several years.The Cost of Homeownership

How much goes or should go into a down payment? On average, how much can you expect to spend on utilities on a monthly basis? Here are some important things to consider when calculating the real cost of homeownership.

Wednesday, October 24, 2018

Still Think You Need 15-20% Down to Buy a Home? Think Again!

According to a new study from Urban Institute, there are over 19 million millennials in 31 cities who are not only ready and willing to become homeowners, but are able to as well!

Now that the largest generation since baby boomers has aged into prime homebuying age, there will no doubt be an uptick in the national homeownership rate. The study from Urban Institute revealed that nearly a quarter of this generation has the credit and income needed to purchase a home.

Surprisingly, the largest share of mortgage-ready millennials lives in expensive coastal cities. These cities often attract highly skilled workers who demand higher salaries for their expertise.

So, what’s holding these mortgage-ready millennials back from buying?

Myths About Down Payment Requirements!

Most of the millennials surveyed for the study believe that they need at least a 15% down payment in order to buy a home when, in reality, the median down payment in the US in 2017 was just 5%, and many programs are available for even lower down payments!The study goes on to point out that:

“Despite limited awareness, every state has programs that provide grants and loans to make homeownership more attainable, with average assistance in various states ranging from $2,436 to $21,171.”

Bottom Line

With so many young families now able to buy a home in today’s market, the demand for housing will continue for years to come. If you are one of the many millennials who have questions about their ability to buy in today’s market, sit with a local real estate professional who can assist you along your journey!Tuesday, October 23, 2018

Housing Is Still Affordable in the United States!

Lately, there have been many headlines circulating about whether or not there is an “affordability issue forming in the housing market.”

If you are considering selling your current house and moving up to the home of your dreams, but are unsure whether or not to believe what you’re seeing in the news, let’s look at the results of the latest Housing Affordability Report from the National Association of Realtors (NAR).

According to NAR:

“A value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home. An index above 100 signifies that a family earning the median income has more than enough income to qualify for a mortgage loan on a median-priced home, assuming a 20 percent down payment.”

- The national index results for August came in at 141.2.

- This is up from 138.9 in July, but down 8.3% from last August’s value of 153.9.

With an index reading of 141.2, housing remains affordable in the U.S.

Regionally, affordability is up in three out of four regions. The Northeast had the biggest gain at 6.2%. The South had an increase of 2.4% followed by the West with a slight increase of 0.1%. The Midwest had the only dip in affordability at 4.8%.

Despite month-over-month changes, the most affordable region remains the Midwest, with an index value of 175.7. The West remains the least affordable region at 101.2. For comparison, the index was 146.7 in the South, and 151.2 in the Northeast.

Bottom Line

If you are thinking of selling your home, contact a local real estate professional who can help you understand the affordability conditions in your marketplace.Monday, October 22, 2018

Will Home Prices Continue to Increase?

There are many unsubstantiated theories about what is happening with home prices. From those who are worried that prices are falling (data shows this is untrue), to those who are concerned that prices are again approaching boom peaks because of “irrational exuberance” (this is also untrue as prices are not at peak levels when they are adjusted for inflation), there seems to be no shortage of opinion.

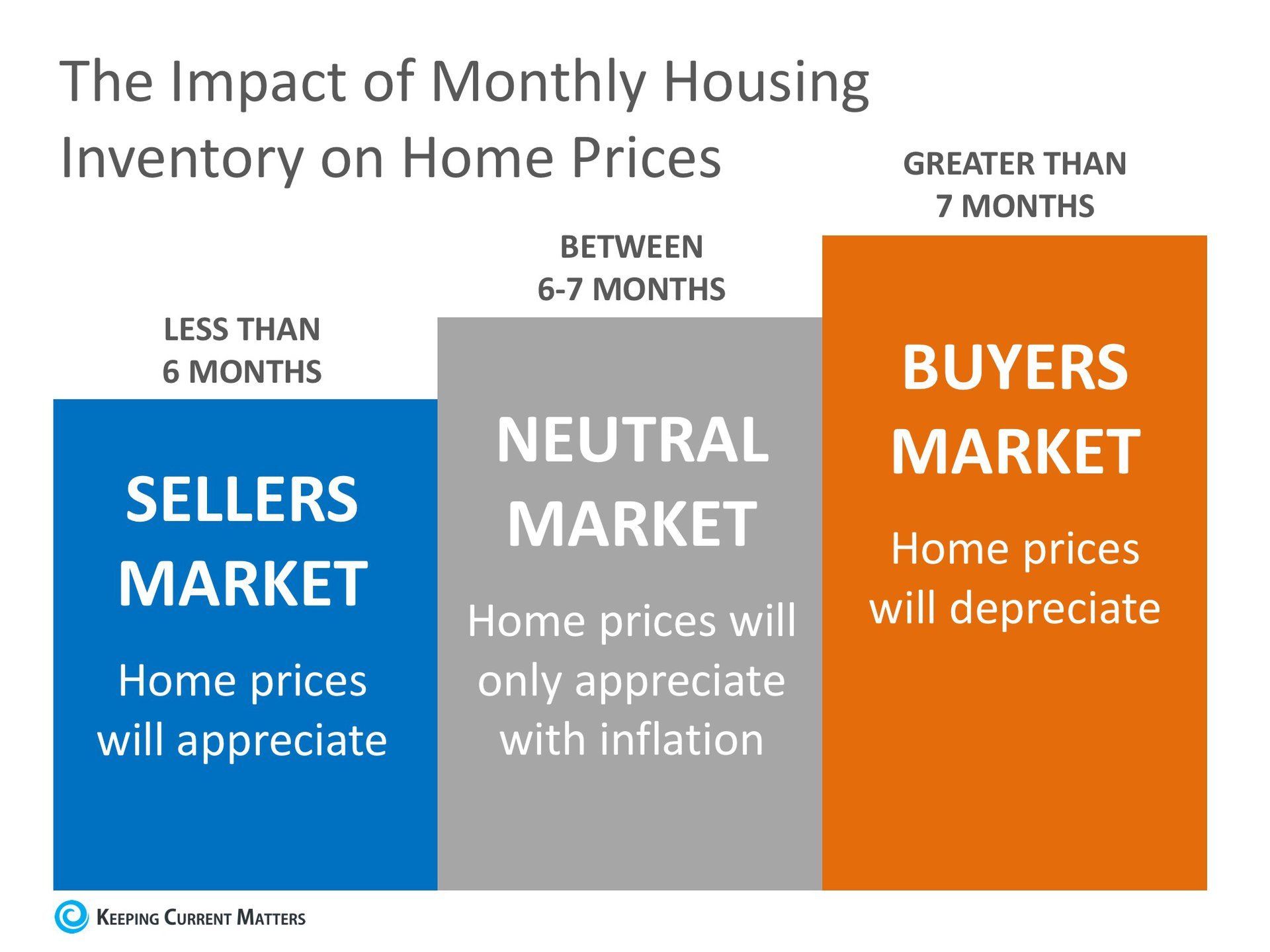

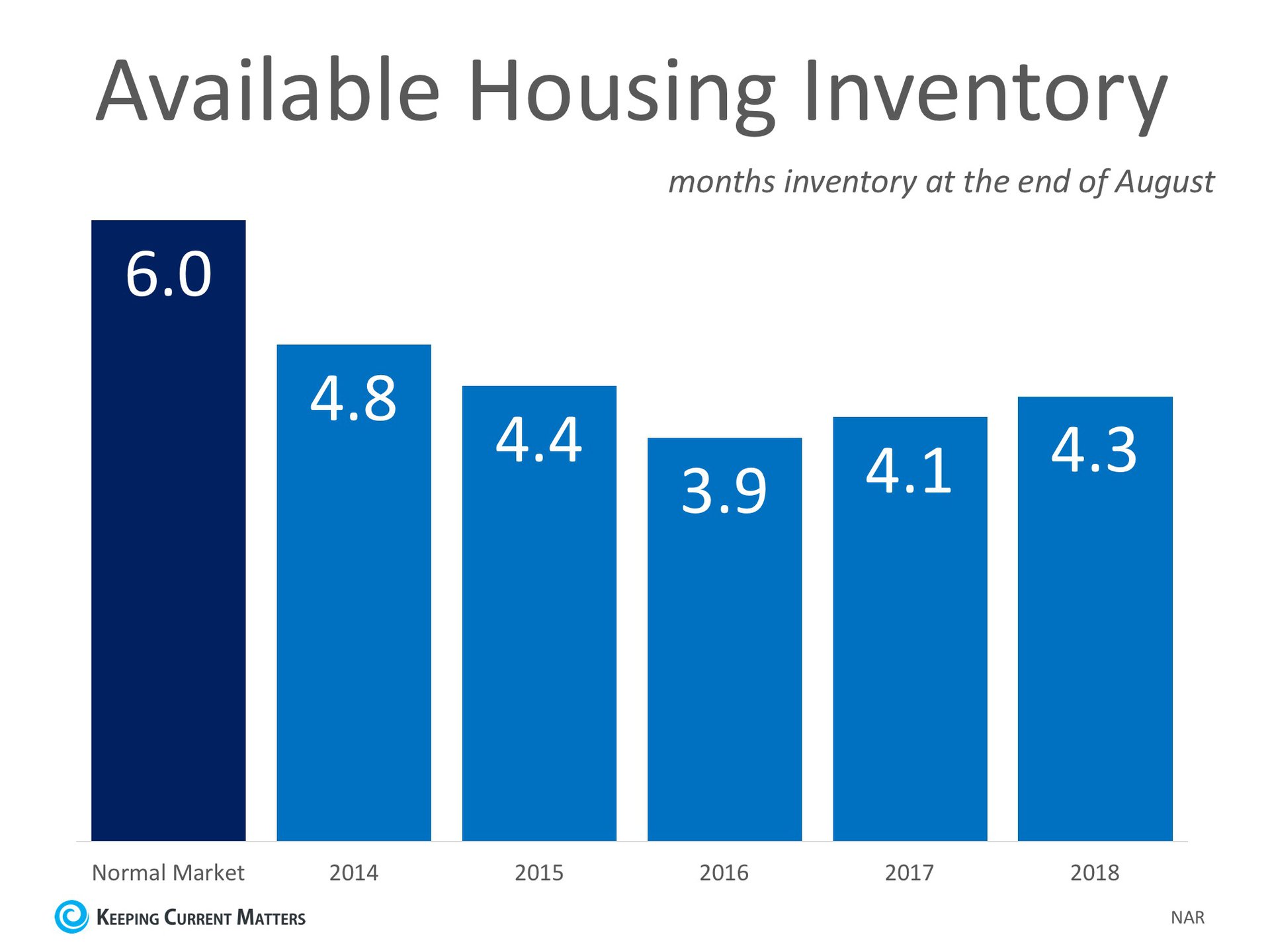

However, the increase in prices is easily explained by the theory of supply & demand. Whenever there is a limited supply of an item that is in high demand, prices increase. It is that simple. In real estate, it takes a six-month supply of existing salable inventory to maintain pricing stability. In most housing markets, anything less than six months will cause home values to appreciate and anything greater than seven months will cause prices to depreciate (see chart below).

According to the Existing Home Sales Report from the National Association of Realtors (NAR), the monthly inventory of homes for sale has been below six months for the last five years (see chart below).

Bottom Line

If buyer demand continues to outpace the current supply of existing homes for sale, prices will continue to appreciate. Nothing nefarious is taking place. It is simply the theory of supply & demand working as it should.Friday, October 19, 2018

What to Plant in Your Garden This Fall

The cool temperatures that come with fall make it a great time to get outside and enjoy the crisp and cool air. Fall introduces the potential for all different types of flowers, vegetables and more to thrive in your garden this season. Whether you’re looking for a pop of color or trying to add to your vegetable garden, here’s everything you know about what to plant this season.

Diversify Your Vegetables

Timing is key when planting vegetables in the fall. Most fall vegetables should be planted while the weather is still warm to allow their roots to grow and mature before the soil gets too cold. Luckily, there are many different types of vegetables that are hearty enough to grow in cooler weather, especially in the Southeast. Beets, broccoli, cabbage, cauliflower, lettuce, radish, spinach and kale are all great options that grow well towards the end of the year.

Plant Fall Flowers

If you’re looking to plant a flower that will bloom in the fall, pansies are a great option. Pansies are perennials, so they will bloom in both the fall and spring, giving you two seasons of fantastic colors. Another flower that is great for fall is the chrysanthemum, which blooms stunning golden, orange and white colors. For flowers that will be ready to bloom in later seasons, try planting daffodils, grape hyacinth or peonies. Planting these in the fall will ensure that your yard will be filled with color come spring.

Garden with Green

Want to add some greenery to your yard? Hostas are hearty plants that stay green year round and grow quickly in a variety of climates. Another evergreen plant to consider are ferns. These plants thrive in shaded areas, away from direct sunlight. If you are considering establishing new grass in your yard, autumn is a perfect time. The hot and dry summer heat is over and weather conditions are perfect to seed or re-seed your yard. The cooler temperatures will help keep moisture locked in, and the soil will still be warm enough to help foster healthy roots.

Add Style and Privacy

The best time to plant trees and shrubs is in the fall. The soil is still warm but the air is cooler, making it the optimal time for roots to grow. Japanese maple trees have beautiful autumn-colored leaves that will last all year long and Gingko trees have fantastic golden leaves that will be sure to highlight your yard. If you’re looking to make your yard seem fuller and more private, shrubs and hedges are perfect to add, as they typically stay green throughout the entire year and can withstand light frosts. For fall-colored shrubs, try Chinese loropetalum, a shrub filled with rich-colored burgundy leaves, or burning bush, a gorgeous red shrub that needs very little care or upkeep, and is resistant to harsh weather.

Try adding a variety of these plants to your yard or garden this fall, and keep your home looking green and healthy all year long.

Thursday, October 18, 2018

Is the Increase in Inventory a Bullish or Bearish Sign for Real Estate?

In a recent article, National Housing Inventory Crisis Reaches Inflection Point, realtor.com reported that:

-

- New listings jumped 8% year-over-year nationally, the largest increase since 2013

- Total listings in the 45 largest markets are now up 6% on average over last year

“With the rate of home price appreciation starting to decelerate alongside the uptick in inventory, we expect significant debate whether this is a bullish or bearish sign.”

Is this a sign the market might crash?

There are those who look at the increase in inventory as a sign that we are returning to the market we saw last decade. However, a closer look shows that we are nowhere near the levels of inventory we reached before the crash in 2008.A normal market would have about 6-months inventory, but the latest Existing Home Sales Report issued by the National Association of Realtors revealed that:

“Unsold inventory is at a 4.3-month supply at the current sales pace up from 4.1 months a year ago.”A decade ago, prices began to rapidly depreciate in June 2007. At that time, we had a 9.1-month supply (more than double what it is today) and inventory kept rising until it hit a peak of 11.1 months in April of 2008.

With the current levels of buyer demand, any such increase in months supply is highly unlikely. As Danielle Hale, realtor.com’s Chief Economist explains:

“After years of record-breaking inventory declines, September’s almost flat inventory signals a big change in the real estate market. Would-be buyers who had been waiting for a bigger selection of homes for sale may finally see more listings materialize. But don’t expect the level to jump dramatically.

Plenty of buyers in the market are scooping up homes as soon as they’re listed, which will keep national increases relatively small for the time being.”

What will be the result of the increase in inventory?

The increase in inventory will allow many families who had been unable to find a home to finally become homeowners. Again, we quote from the ‘Z Report’:“In our view, the short-term narrative will probably be confusing, but more sustainable growth and affordability will likely be the end result.”

Bottom Line

If you are either a first-time or second-time buyer who has given up, check with a local real estate professional to see if new listings have come to the market in your area.Wednesday, October 17, 2018

Tuesday, October 16, 2018

Baby Boomers are Downsizing, Are You Ready to Move?

For a while now baby boomers have been

blamed for a portion of the housing market’s current lack of housing

inventory, but should they really be getting the blame?

Here’s what some of the experts have to say on the subject:

Aaron Terrazas, Senior Economist at Zillow, says that “Boomers are healthier and working longer than previous generations, which means they aren’t yet ready to sell their homes.”

According to a study by Realtor.com, 85% of baby boomers indicated they were not planning to sell their homes.

It is true that baby boomers are healthier

and are thus working and living longer, but are they also refusing to

sell their homes?

Last month, Trulia looked at the housing situation of seniors (aged 65+) today compared to that of a decade ago. Trulia’s study revealed that:

“Although seniors appear to be delaying downsizing until later in life, as a group, households 65 and over are still downsizing at roughly the same rate as in years past.”

Trulia also explains that,

“5.5% of households 65 and over moved, pretty evenly split between moves to single family (2.7%) and multifamily (2.4%) homes. In 2005, these percentages were virtually the same, with 5.5% of senior households moving, including 2.5% into single family and 2.5% into multifamily homes.”

So, if these percentages are the same, what is the challenge?

Recent reports tell us that the older population grew from 3 million in 1900 to 47.8 million in 2017.

In addition, the Census recently revised the numbers from their National Population Projections:

“The aging of baby boomers means that within just a couple decades, older people are projected to outnumber children for the first time in U.S. history…By 2035, there will be 78.0 million people 65 years and older compared to 76.7 million under the age of 18.”

Bottom Line

If you are a baby boomer who is not sure

whether you should downsize or move to a warmer climate (other people

are doing it, why not you?), call a local real estate professional who

can help you evaluate your options today!

Monday, October 15, 2018

Pre-Approval: Your 1st Step in Buying a Home

In many markets across the country, the number of buyers searching for their dream homes outnumbers the number of homes for sale. This has led to a competitive marketplace where buyers often need to stand out. One way to show you are serious about buying your dream home is to get pre-qualified or pre-approved for a mortgage before starting your search.

Even if you are in a market that is not as competitive, understanding your budget will give you the confidence of knowing if your dream home is within your reach.

Freddie Mac lays out the advantages of pre-approval in the ‘My Home’ section of their website:

“It’s highly recommended that you work with your lender to get pre-approved before you begin house hunting. Pre-approval will tell you how much home you can afford and can help you move faster, and with greater confidence, in competitive markets.”One of the many advantages of working with a local real estate professional is that many have relationships with lenders who will be able to help you through this process. Once you have selected a lender, you will need to fill out their loan application and provide them with important information regarding “your credit, debt, work history, down payment and residential history.”

Freddie Mac describes the ‘4 Cs’ that help determine the amount you will be qualified to borrow:

- Capacity: Your current and future ability to make your payments

- Capital or cash reserves: The money, savings, and investments you have that can be sold quickly for cash

- Collateral: The home, or type of home, that you would like to purchase

- Credit: Your history of paying bills and other debts on time

Bottom Line

Many potential homebuyers overestimate the down payment and credit scores necessary to qualify for a mortgage today. If you are ready and willing to buy, you may be pleasantly surprised at your ability to do so.Friday, October 12, 2018

Thursday, October 11, 2018

Fast Track Rental Property

FHA allows owner-occupants to purchase up to a four-unit property with a minimum 3.5% down payment. The rent collected on three units could be used to make the payment and the owners' pro-rata share would be less than ¼ of the payment itself.

The owner-occupied unit would be considered their principal residence. The other three units are treated as rental property and eligible for cost recovery, a non-cash deduction plus all the normal business expenses. The rental income of the three remaining units is calculated as income and assists the buyer in qualifying.

A homeowner could buy a four-unit, live in one for two years, buy another four-unit with a minimum down payment, move into one unit, rent the other three as well as the previous unit in the first property. Then, after another two years, repeat the same process over again.

The fifth year, the homeowner/investor would have a total of 11 rental units plus the one that they are occupying. An acquisition strategy like this might be difficult for a family with children and a single person or couple might find it easier to move more frequently.

As the equity increases in these properties, due to appreciation and amortization, the money could be pulled out through refinancing to purchase additional income properties. Another objective might be to pay the mortgage off as soon as possible and any cash flow after tax could be applied directly to the principal.

FHA has a nationwide mortgage limit for a four-unit of $521,250 but some high-cost areas have been designated with increased limits. There are also loan programs for two and three-unit properties with limits of $347,000 and $419,425 with similar exceptions for high-cost areas.

The low mortgage rate and minimal down payments for owner-occupied FHA mortgages makes this strategy attractive because it gives investors an opportunity to highly leverage their investment. Most non-owner-occupied (investor) mortgages would require 20-25% down payment and have a slightly higher interest rate than for an owner-occupant.

Wednesday, October 10, 2018

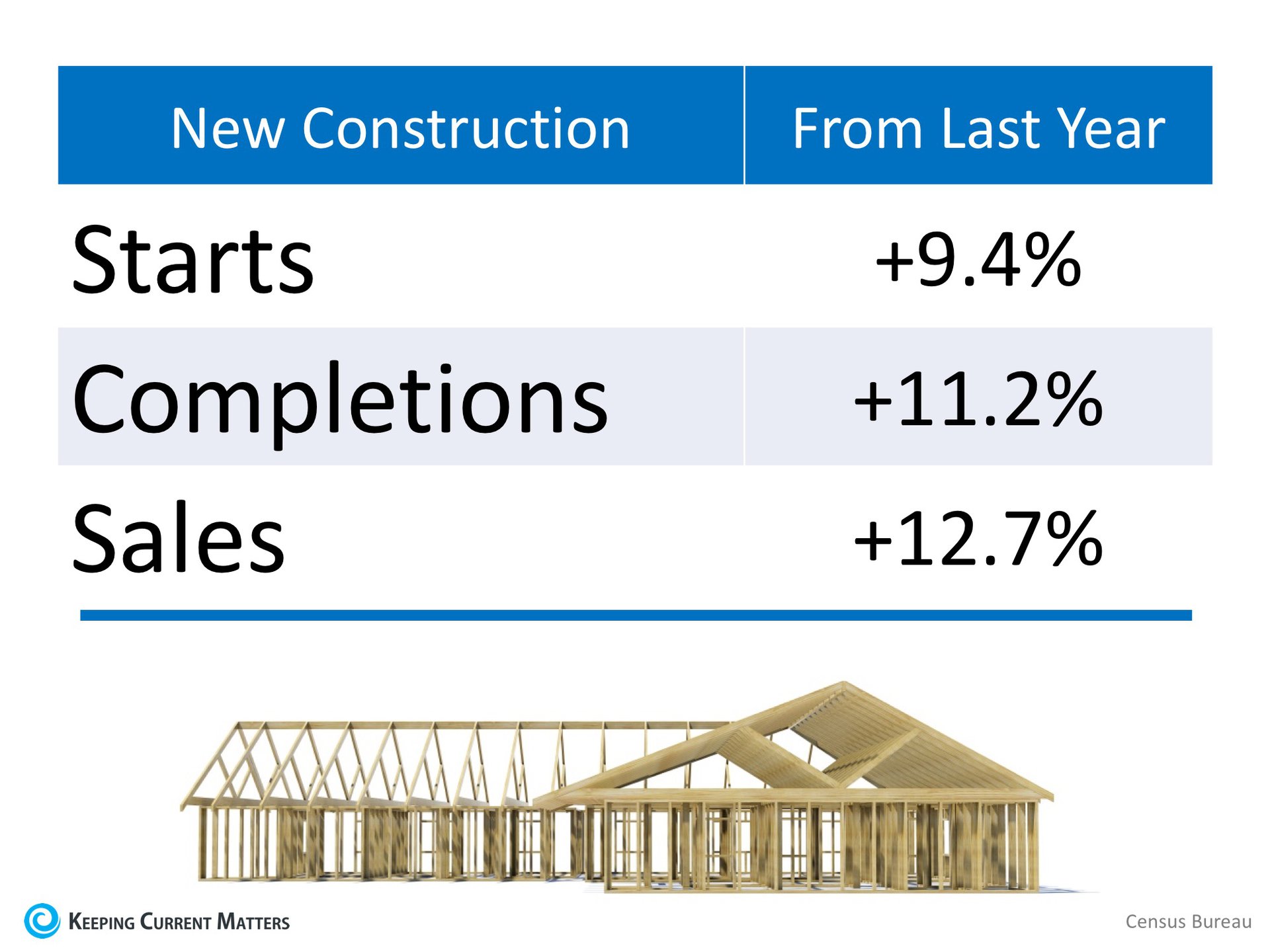

New Home Sales Up 12.7% From Last Year

According to the latest New Residential Sales Report from the Census Bureau, new construction sales in August were up 3.5% from July and 12.7% from last year! This marks the second consecutive month with double-digit year-over-year growth (12.8% in July).

The report also showed that builders have ramped up construction with an increase in new construction starts and completions. The summer months are often a busy time for builders as they capitalize on the warmer weather to be able to finish projects.

Below is a table showing the change in starts, completions, and sales from last August.

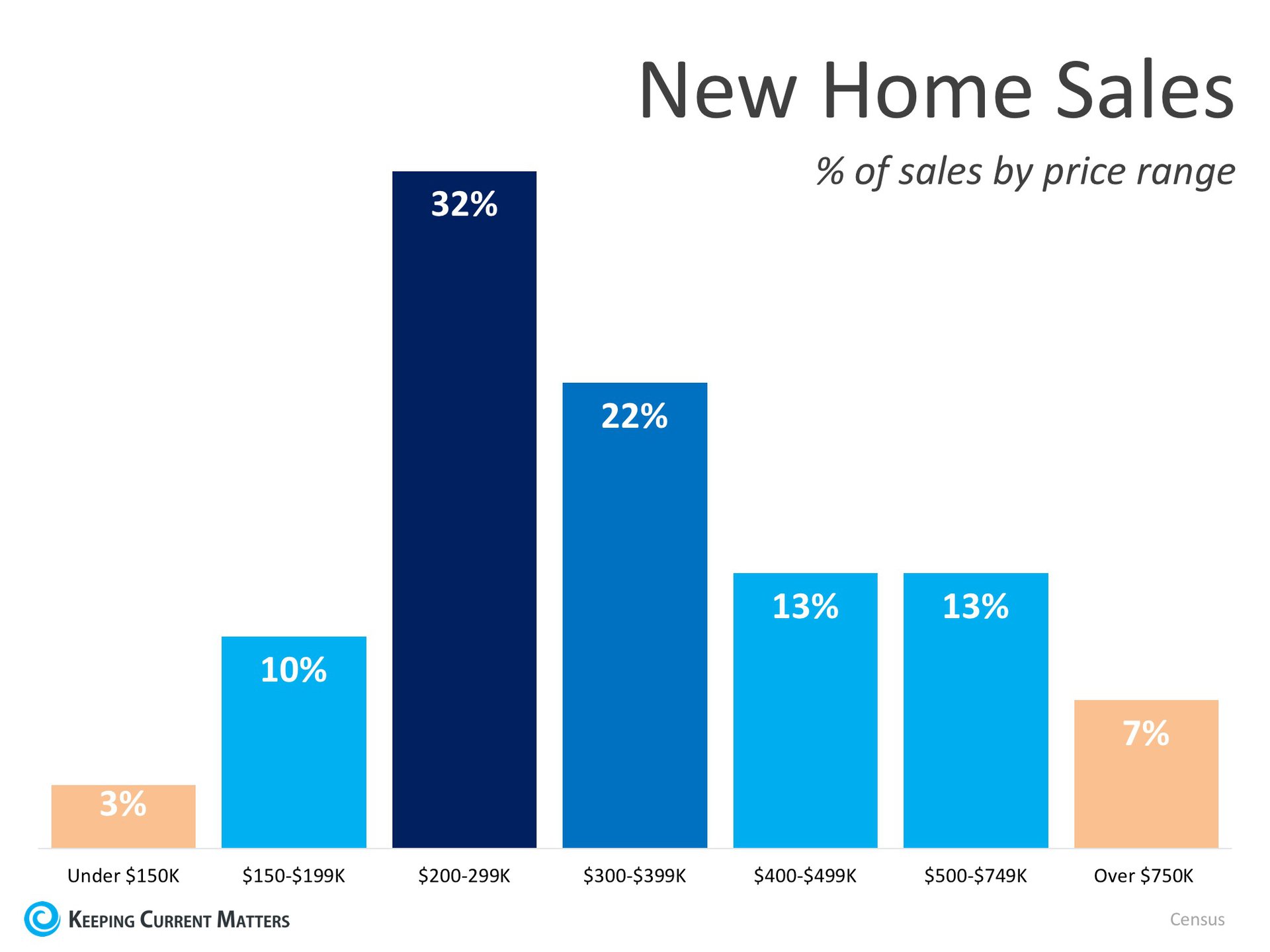

Other notable news from the report is that the percentage of new construction sales in the $200-$299k range has continued to break away from the $300-$399k range.

This shows that builders are starting to build lower-priced homes that will help alleviate some of the inventory challenges in the starter and trade-up home categories. The chart below shows the full breakdown.

What does this mean for buyers and sellers?

If you are thinking of buying or selling in today’s market, you no doubt have heard that there is a shortage of existing homes for sale which has been driving home prices up across the country. The additional new construction coming to the market could help alleviate this shortage, but we are still not back up to pre-crisis levels.Tuesday, October 9, 2018

What's Going On With Home Prices?

According to CoreLogic’s latest Home Price Insights Report, national home prices in August were up 5.5% from August 2017. This marks the first time since June 2016 that home prices did not appreciate by at least 6.0% year-over-year.

CoreLogic’s Chief Economist Frank Nothaft gave some insight into this change,

“The rise in mortgage rates this summer to their highest level in seven years has made it more difficult for potential buyers to afford a home. The slackening in demand is reflected in the slowing of national appreciation, as illustrated in the CoreLogic Home Price Index.One of the major factors that has driven prices to accelerate at a pace of between 6-7% over the past two years was the lack of inventory available for sale in many areas of the country. This made houses a prized commodity which forced many buyers into bidding wars and drove prices even higher.

National appreciation in August was the slowest in nearly two years, and we expect appreciation to slow further in the coming year.”

According to the National Association of Realtors’ (NAR) latest Existing Home Sales Report, we are starting to see more inventory come to market over the last few months. This, paired with patient buyers who are willing to wait to find the right homes, is creating a natural environment for price growth to slow.

Historically, prices appreciated at a rate of 3.7% (from 1987-1999). CoreLogic predicts that prices will continue to rise over the next year at a rate of 4.7%.

Bottom Line

As the housing market moves closer to a ‘normal market’ with more inventory for buyers to choose from, home prices will start to appreciate at a more ‘normal’ level, and that’s ok! If you are curious about home prices in your area, talk to a local real estate professional who can show you what’s going on!Monday, October 8, 2018

The True Cost of NOT Owning Your Home

Realtor.com reported that:

“Buying remains the more attractive option in the long term – that remains the American dream, and it’s true in many markets where renting has become really the shortsighted option…as people get more savings in their pockets, buying becomes the better option.”

What proof exists that owning is financially better than renting?

1. In a previous blog, we highlighted the top 5 financial benefits of homeownership:- Homeownership is a form of forced savings.

- Homeownership provides tax savings.

- Homeownership allows you to lock in your monthly housing cost.

- Buying a home is cheaper than renting.

- No other investment lets you live inside of it.

3. Less than a month ago, we explained that a family that purchased an average-priced home at the beginning of 2018 could build more than $49,000 in family wealth over the next five years.

4. Some argue that renting eliminates the cost of taxes and home repairs, but every potential renter must realize that all the expenses the landlord incurs are already baked into the rent payment – along with a profit margin!

Bottom Line

Owning your home has many social and financial benefits that cannot be achieved by renting.Friday, October 5, 2018

Thursday, October 4, 2018

Mortgage Free

Mortgage Free

It may be an all too common belief that a person will have a house payment and a car payment for the rest of their lives. However, with a plan and some determination, you can be mortgage free.

Planning for retirement is obviously important and many times, an activity plagued by procrastination. Some homeowners' goal is to have their home paid for by retirement, so they won't have payments. It makes sense to eliminate a sizable recurring expense before they quit working.

By making regular principal contributions in addition to the payments, the debt can be eliminated by the target retirement date.

Assume a homeowner refinanced their $300,000 mortgage at 4% last year for 30 years with the first payment due on May 1, 2017. With normal amortization, the home will be paid for at the end of the term.

Additional principal contributions with each payment will save interest, build equity and of course, accelerate the payoff on the home. An extra $250.00 a month would pay off the mortgage 7.5 years sooner. $786.81 extra with each payment would pay off the loan in 15 years.

Having a home paid for at retirement has the apparent benefit of no house payment. A debt-free home is also a substantial asset that could be borrowed against or sold if unanticipated events should occur.

Wednesday, October 3, 2018

2 Factors to Watch in Today's Real Estate Market Whether Buying or Selling

When it comes to buying or selling a home there are many factors you should consider. Where you want to live, why you want to buy or sell, and who will help you along your journey are just some of those factors. When it comes to today’s real estate market, though, the top two factors to consider are what’s happening with interest rates & inventory.

Interest Rates

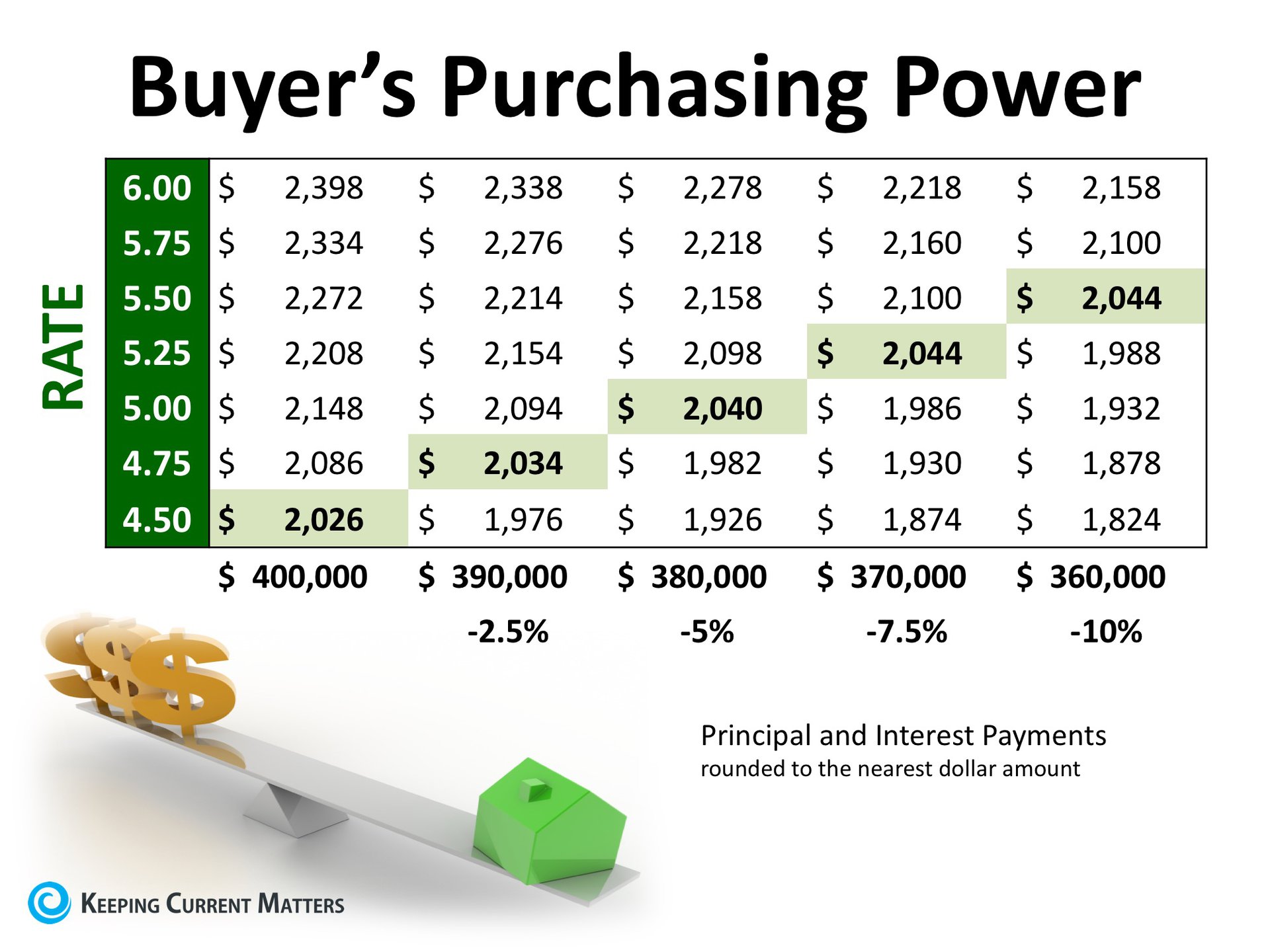

Mortgage interest rates have been on the rise and are now over three-quarters of a percentage point higher than they were at the beginning of the year. According to Freddie Mac’s latest Primary Mortgage Market Survey, rates climbed to 4.72% for a 30-year fixed rate mortgage last week.The interest rate you secure when buying a home not only greatly impacts your monthly housing costs, but also impacts your purchasing power.

Purchasing power, simply put, is the amount of home you can afford to buy for the budget you have available to spend. As rates increase, the price of the house you can afford to buy will decrease if you plan to stay within a certain monthly housing budget.

The chart below shows the impact that rising interest rates would have if you planned to purchase a $400,000 home while keeping your principal and interest payments between $2,020-$2,050 a month.

With each quarter of a percent increase in interest rate, the value of the home you can afford decreases by 2.5% (in this example, $10,000). Experts predict that mortgage rates will be over 5% by this time next year.

Inventory

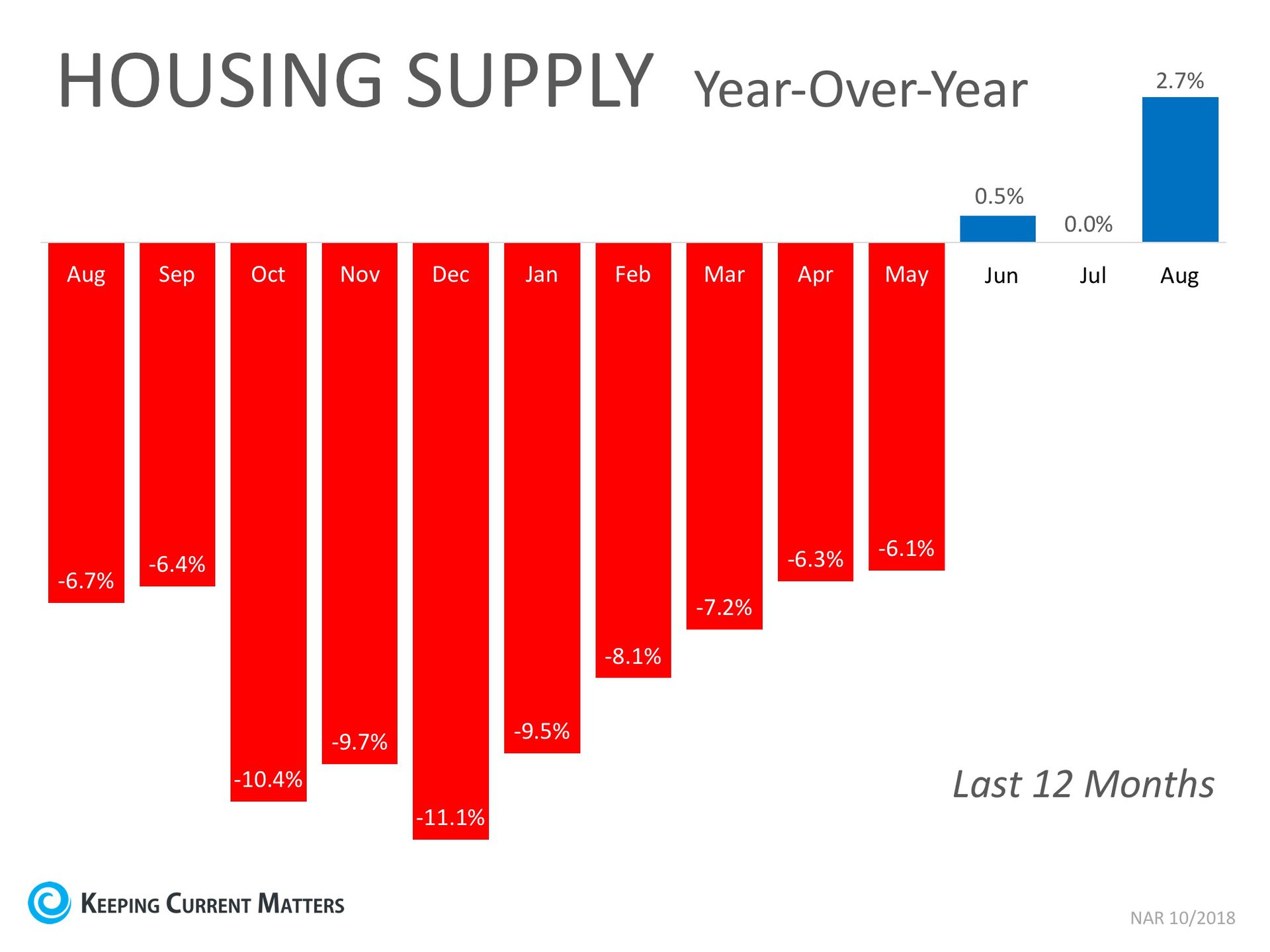

A ‘normal’ real estate market requires there to be a 6-month supply of homes for sale in order for prices to increase only with inflation. According to the National Association of Realtors (NAR), listing inventory is currently at a 4.3-month supply (still well below the 6-months needed), which has put upward pressure on home prices. Home prices have increased year-over-year for the last 78 straight months.The inventory of homes for sale in the real estate market had been on a steady decline and experienced year-over-year drops for 36 straight months (from July 2015 to May 2018), but we are starting to see a shift in inventory over the last three months.

The chart below shows the change in housing supply over the last 12 months compared to the previous 12 months. As you can see, in June, July, and August, inventory levels have started to increase as compared to the same time last year.

This is a trend to watch as we move further into the fall and winter months. If we continue to see an increase in homes for sale, we could start moving further away from a seller’s market and closer to a normal market.

Bottom Line

If you are planning to enter the housing market, either as a buyer or a seller, make sure that you have an experienced local agent who can help you navigate the changes in mortgage interest rates and inventory.Tuesday, October 2, 2018

Mortgage Interest Rates are Still Going Up... Should You Wait to Buy?

In addition to the predictions from the four major reporting agencies mentioned above, the Federal Open Market Committee recently voted “unanimously to approve a 1/4 percentage point increase in the primary credit rate to 2.75 percent.” Historically, an increase in the primary credit rate has translated to an overall jump in mortgage interest rates as well.

This has caused some purchasers to lament the fact that they may no longer be able to get a rate below 4%. However, we must realize that current rates are still at historic lows.

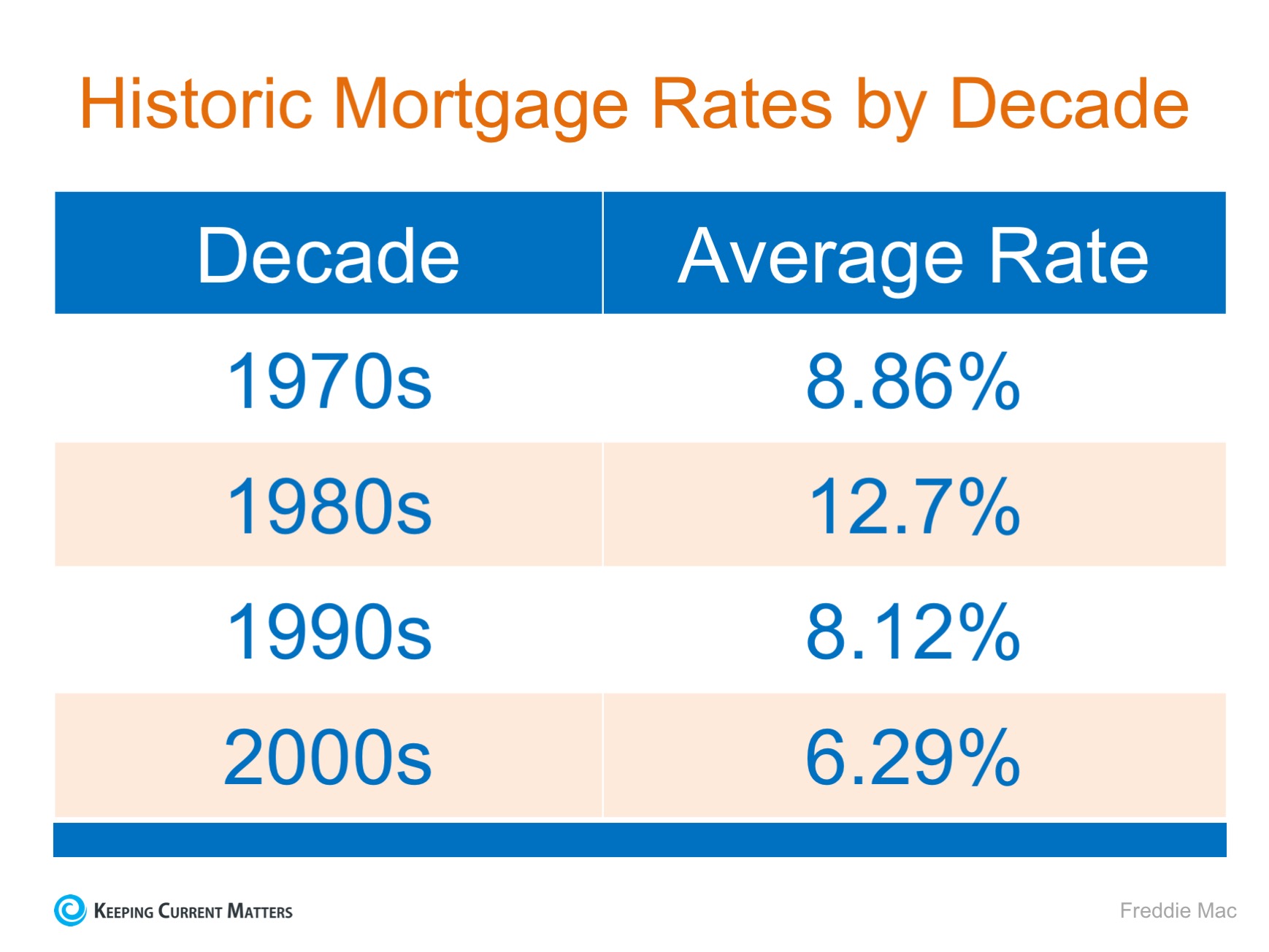

Here is a chart showing the average mortgage interest rate over the last several decades:

Bottom Line

Though you may have missed the lowest mortgage rate ever offered, you can still get a better interest rate than your older brother or sister did ten years ago, a lower rate than your parents did twenty years ago, and a better rate than your grandparents did forty years ago.

Subscribe to:

Comments (Atom)