Buying your first home can be a bit intimidating but it doesn't have to be! Contact me today and I can walk you through the process.

"Dated kitchens--just like bathrooms--are a major barrier for resale. Buyers want modern amenities and styling, and most aren't interested in renovating post-purchase."

"Eighty-two percent of homeowners said their updated kitchen gave them a greater desire to be at home, and 95% were happy or satisfied with the result."

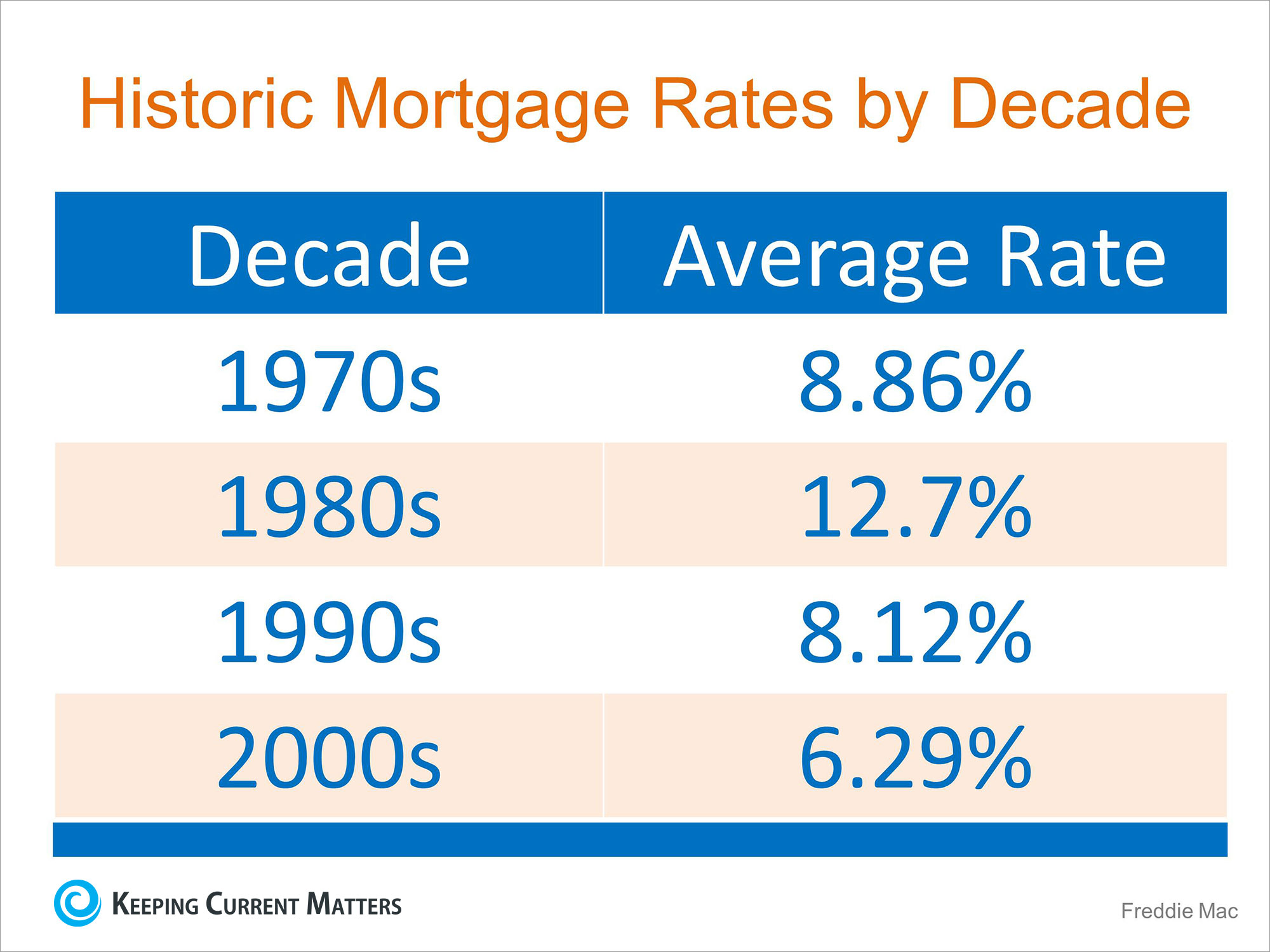

Even though rates are closer to 4% than they have been in nearly 6 months, they are still slightly below where we started 2016, at 3.97%. The great news is that even at 4%, rates are still significantly lower than they have been over the last 4 decades, as you can see in the chart below.

Any increase in interest rate will impact your monthly housing costs when you secure a mortgage to buy your home. A recent Wall Street Journal article points out that,"While still only roughly half the average over the past 45 years, according to Freddie Mac, the quick rise has lenders worried that home loans could become more expensive far sooner than anticipated." Tom Simons, a Senior Economist at Jefferies LLC, touched on another possible outcome for higher rates:"First-time buyers look at the monthly total, at what they can afford, so if the mortgage is eaten up by a higher interest expense then there's less left over for price, for the principal. Buyers will be shopping in a lower price bracket; thus demand could shift a bit."

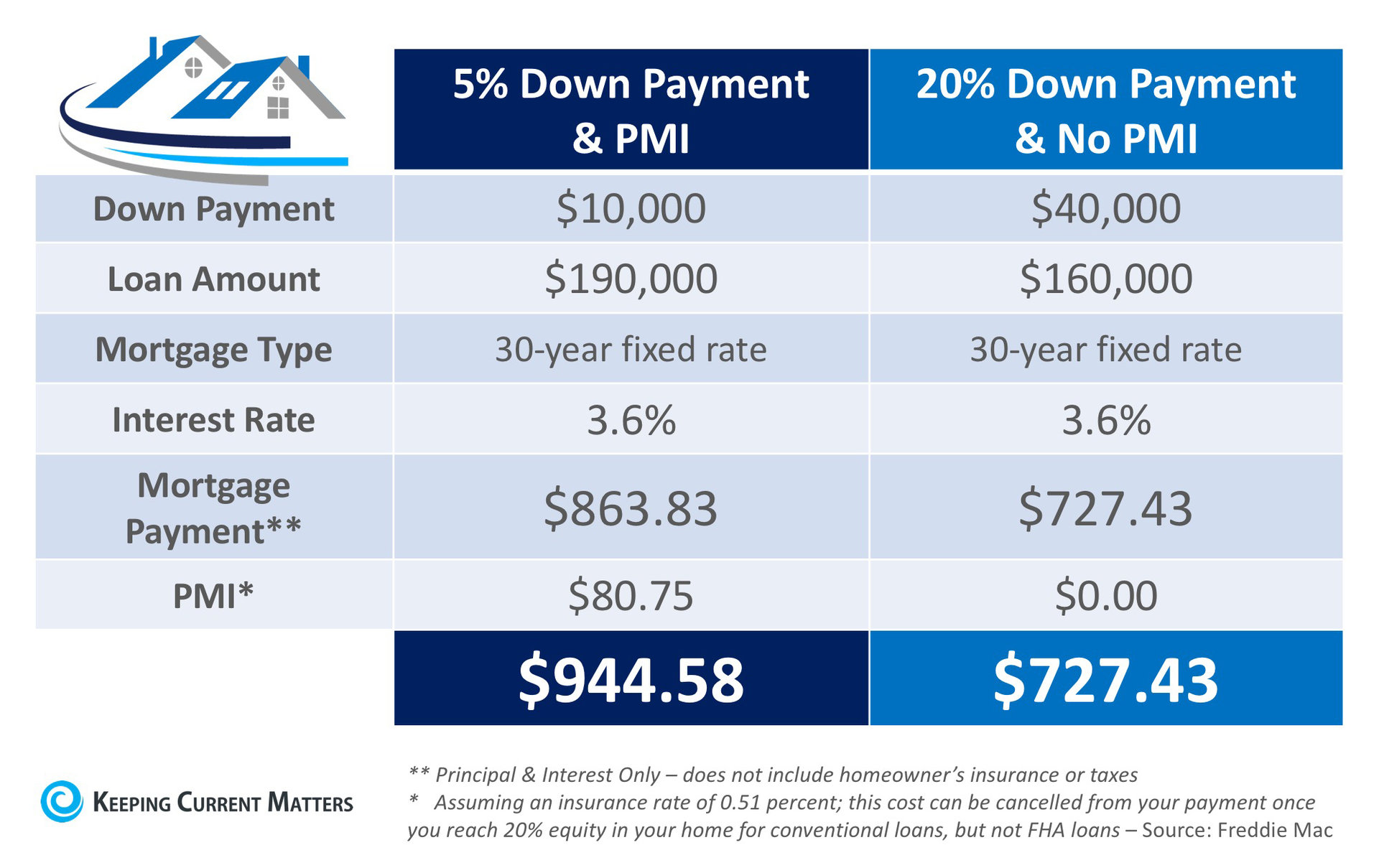

"An insurance policy that protects the lender if you are unable to pay your mortgage. It's a monthly fee, rolled into your mortgage payment, that is required for all conforming, conventional loans that have down payments less than 20%. Once you've built equity of 20% in your home, you can cancel your PMI and remove that expense from your mortgage payment."As the borrower, you pay the monthly premiums for the insurance policy, and the lender is the beneficiary. Freddie Mac goes on to explain that:

"The cost of PMI varies based on your loan-to-value ratio - the amount you owe on your mortgage compared to its value - and credit score, but you can expect to pay between $30 and $70 per month for every $100,000 borrowed."According to the National Association of Realtors, the average down payment for all buyers last year was 10%. For first-time buyers, that number dropped to 6%, while repeat buyers put down 14% (no doubt aided by the sale of their home). This just goes to show that for a large number of buyers last year, PMI did not stop them from buying their dream homes. Here's an example of the cost of a mortgage on a $200,000 home with a 5% down payment & PMI, compared to a 20% down payment without PMI:

"It's no doubt an added cost, but it's enabling you to buy now and begin building equity versus waiting 5 to 10 years to build enough savings for a 20% down payment."

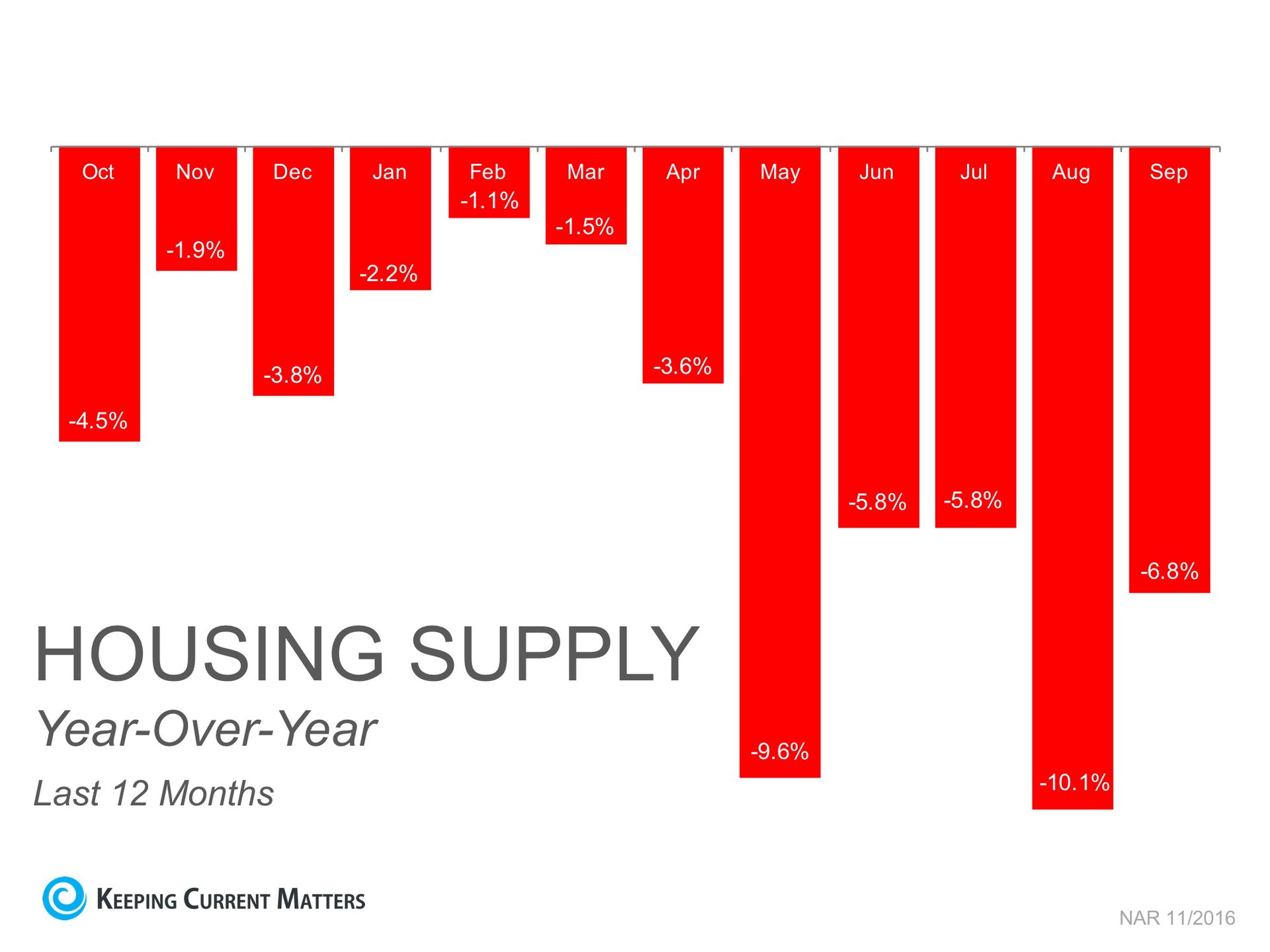

"Overall, the fundamental trends we have been seeing all year remain solidly in place as we enter the traditionally slower sales season, and pent-up demand remains substantial as buyers seek to get a home under contract while rates remain so low."NAR's Chief Economist, Lawrence Yun, points out that the inventory shortage we are currently experiencing isn't a new challenge by any means:

"Inventory has been extremely tight all year and is unlikely to improve now that the seasonal decline in listings is about to kick in. Unfortunately, there won't be much relief from new home construction, which continues to be grossly inadequate in relation to demand."

"Even though the value of the average home in the U.S. increased by about $13,500 over the last year, thanks to declining interest rates it actually costs almost exactly the same in principal and interest each month to purchase as it did this time last year. Even taking into account the fact that affordability can vary - sometimes significantly - across the country based upon the different rates of home price appreciation we're seeing, that's a pretty incredible balancing act between interest rates and home prices at the national level... Right now, it takes 20 percent of the median monthly income to cover monthly payments on the median-priced home, which is well below historical norms." However, the report warns that affordability will be dramatically impacted by an increase in mortgage rates. "A half-point increase in interest rates would be equivalent to a $17,000 jump in the average home price, and bring that ratio to 21.5 percent. This increase is still below historical norms, but puts more pressure on homebuyers."